The Great Leasing v. Buying Debate: EV Edition

September 2024

The decision about whether to lease a car versus buy is a classic conundrum for car buyers. Recently, it’s a discussion that’s been heating up in the EV space, particularly on social media – and due to a loophole in the federal EV tax credit, the answer may be surprising.

Traditionally, the advice to consumers on this debate has been, when you’re able, to buy a car, rather than lease. That’s because by owning the car, you aren’t subject to mileage limits, you can customize your vehicle, and you don’t have to worry about returning it to the dealer in top shape. (Additionally, financing terms are often easier for consumers to navigate than leasing deals). With EVs, this advice is starting to get turned on its head.

What Is This Tax Loophole All About?

Recent federal legislation has encouraged both buyers and lessees to seriously consider EVs as their next car. As part of the Inflation Reduction Act, signed in 2022, the “new clean vehicle” tax credit offers a $7,500 tax break for consumers who buy a new EV. However, EV lessees are also able to access the credit through a different mechanism known as the “qualified commercial clean vehicles” tax credit. In fact, since this credit does not entail strict requirements around manufacturing, sticker price, or buyer income, among other factors, it’s far easier for many lessees to access the benefit.

How it works: Under the IRA, the business that purchases the EV can qualify for the full $7,500 EV tax credit. Leasing agencies purchase EVs from the manufacturer as a commercial sale, which bypasses the tax credit restrictions. The leasing agency is then able to pass these savings along to the consumer in a lease.

This loophole has resulted in a major uptick in EV leasing: As of Q1 2024, about 35% of new EVs were leased, compared to just 12% in 2023.

What Do I Need to Know as a Consumer?

But how do you know if leasing an EV could be the right move for you? Here are some factors to consider:

Pros of Leasing an EV

Easier access to the EV tax credit

- This is especially impactful if you don’t exceed the income thresholds ($150,000 adjusted gross income for single filers and $300,000 for married couples), or are interested in an EV that does not meet the government’s requirements around manufacturing or price.

Try before you buy

- Especially for car shoppers who are on the fence about driving their first EV, leasing is a way of doing a trial run. Compared to purchasing, leasing allows consumers to make a shorter-term decision and less of an upfront commitment, and still have the option to buy out the car in the future.

Access the latest tech

- For tech enthusiasts, who (given where EVs fall on the adoption curve) likely make up the majority of EV owners and lessees, leasing gives you an out in three years, letting you trade up to the latest tech with more advanced features, better battery range, etc.

Pros of Buying an EV

You own the car

- That means, if you’re financing a purchase, your monthly payments end when you pay off the loan. You also are building equity in the car and can one day sell it.

You can take $7,500 off the sticker price

- Assuming you and the EV both meet the qualifications

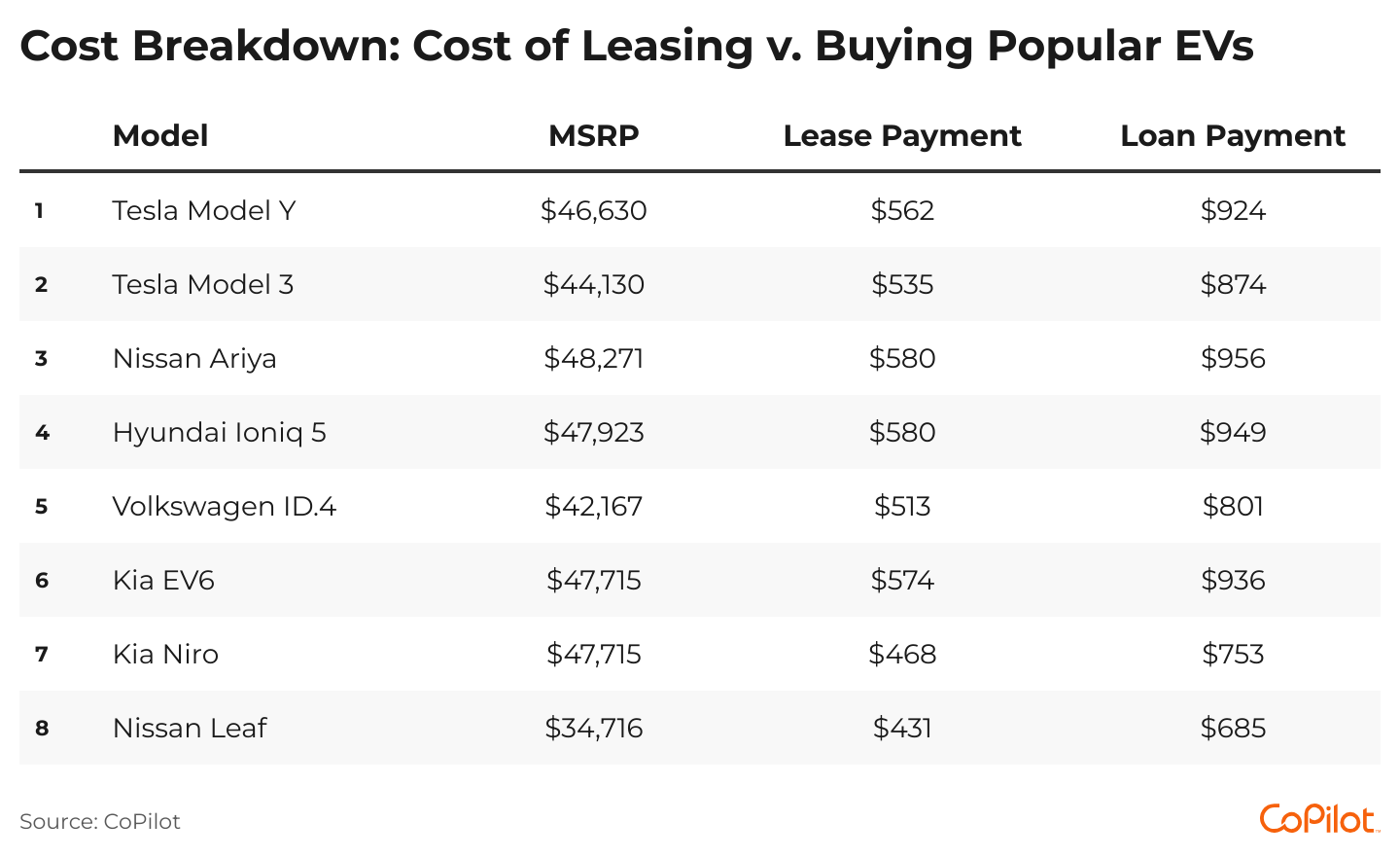

Cost Breakdown: Cost of Leasing v. Buying Popular EVs

Though you of course will not own the EV through leasing, for many popular EVs, leasing often results in the cheaper monthly payment for consumers.

Assumptions:

- $7,500 tax credit applies for both buying and leasing

- Strong credit score

- 48-month loan or lease

- 20% down payment

- 7% sales tax

- Average of 15,000 miles driven per year

Popular Car Searches

Makes

Shop Used Cars

Used Cadillac Truck for Sale Near Me

Used Toyota Truck for Sale Near Me

Used Ford Fiesta for Sale Near Me

Used Ford Transit Cargo Van for Sale Near Newark, NJ

Used Toyota 4Runner for Sale Near Jacksonville, FL

Used Porsche Wagon for Sale Near Me

Used Nissan Sentra for Sale Near Me

Used Nissan GT-R for Sale Near Los Angeles, CA

Used Honda Pilot for Sale Near Des Moines, IA

Used Chrysler Roadster for Sale Near Me

Used Toyota Sequoia for Sale Near Dallas, TX

Used Chevrolet Coupe for Sale Near Me

Used Dodge Wagon for Sale Near Me

Used Infiniti Sedan for Sale Near Me

Used Acura Coupe for Sale Near Me

Used Honda Ridgeline for Sale Near Sacramento, CA

Used Honda Pilot for Sale Near Pompano Beach, FL

Used Toyota Suv for Sale Near Me

Used Kia Hatchback for Sale Near Me

Used Nissan Minivan for Sale Near Me

Used Nissan Rogue for Sale Near Baltimore, MD

Used Honda Ridgeline for Sale Near Me

Used Honda Pilot for Sale Near Me